A number of studies and articles have been appearing since last year questioning the impact of microcredit – microfinance. One of the most recent reports “Does Microcredit Really Help Poor People?” written by the seasoned microfinance expert Richard Rosenberg provides an excellent overview of the studies and his view on this subject. According to this report the claim in doubt is whether microfinance (or the microloans) is the cause for the economic improvement (increase in income and consumption, moving people out of poverty) as well as positive impact in health, education and social empowerment. The problem being that scientific testing of the impact of microcredit is very difficult (and therefore proving the claims are difficult). Rosenberg ends the report with the following words;

“Small one-time subsidies – leverage large multiples of unsubsidized funds – producing sustainable delivery year after year of highly valued services that help hundered of millions of people – keep their consumption stable, finance major expenses, and cope with shocks – despite incomes that are low, irregular, and unreliable.

All and all isn’t this a pretty impressive value proposition, even if we eventually find out that microfinance doesn’t raise income the way some of its proponents have claimed?”

In retrospect, it is very likely that in the past years the rising popularity of microfinance and its impact had become over-blown. Proponents of microfinance (including this author), in their quest of raising awareness of this powerful and effective tool to improve the life of the BOP, have been too enthusiastic and most likely also helped create the overhyped state. So the recent critical articles are deflating the overly high expectations that were built on microfinance and its impact. This is a healthy sign. I thank David Roodman and his excellent open-book blog which has been providing a critical view on the many issues surrounding the impact of microfinance.

On May 12th, Nobel Laureate

On May 12th, Nobel Laureate  I thank Yunus for his wonderful and inspiring work which lead me (and many others) to move from mainstream into the world of social enterprises. I have no doubt that he will continue impacting lives through his work in creating social businesses.

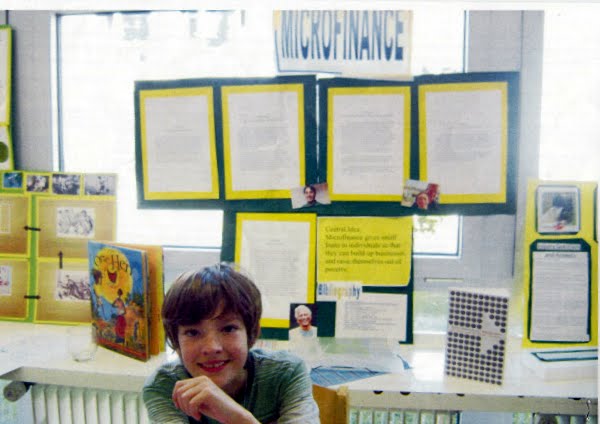

I thank Yunus for his wonderful and inspiring work which lead me (and many others) to move from mainstream into the world of social enterprises. I have no doubt that he will continue impacting lives through his work in creating social businesses. Just two days before, on May 10th, I attended an exhibition on “How I can make a difference” by the 5th graders at the

Just two days before, on May 10th, I attended an exhibition on “How I can make a difference” by the 5th graders at the